Evolution (EVO.ST): The Leader in Live Casino

Thoughts on Evolution (EVO.ST)

Executive Summary

Investors have looked for plenty of ways to get exposure to the de-regulation of the gambling sector in the United States. Swedish company Evolution (EVO.ST) stands out as a high quality way to play the sector, not only for US exposure, but also globally.

Evolution stands out to me for three key reasons:

The business is already highly profitable (yes it actually makes profit and a lot of it). Net profit margins were 50.7% in FY20, and I forecast them to reach 57.5% in FY21e.

Source: Company filings, Gradient estimates 2. As an industry leader in live casino, competitors do not come close to Evolution - in fact, they often copy its successful games. This is due to Evolution’s vastly superior product suite and end customer engagement driven by its highly creative game development team, led by Chief Product Officer, Todd Haushalter.

Personally, I am attracted to industries where profit pools accrue to a limited number of participants within an ecosystem and Evolution ticks this box.

“If you focus exclusively on unfair fights, we focus on economic monopolies and oligopolies, if you focus on unfair fights where companies are always winning, you’re reducing the number of variables”- Yen Liow (emphasis mine)

3. The runway for growth remains attractive as online casinos take further share from land based casinos, with regulation to drive strong growth in the US and Asia. Europe, Evolution’s most mature market, is still expected to grow at ~20% out to 2025, underpinning a robust market outlook.

A traditional DCF model will fade growth, no matter how large the market opportunity or well positioned a company may be. However, if a company’s moat is strong enough (along with its TAM), growth will likely not fade. This provides longer term investors with a significant opportunity.

In this writeup, I will explore why Evolution fits into the above category.

A table of contents is outlined below.

Business Overview

Evolution’s Platform

Evolution’s Moat & Opportunity

The Competition

Regulation

Capital Allocation and Financials

Management & Incentives

Valuation

Where could I be wrong?

Business Overview

Business Snapshot

As the world’s largest online casino supplier, Evolution has a differentiated offering and a high margin cash generative business model.

Industry Map

Evolution is the dominant player in an oligopolistic B2B market.

Revenue Model

Evolution makes money in two main ways – commission fees (variable) and dedicated table fees (fixed). These are paid monthly by operators with typical contracts ~3 years in length.

Commission Fees (Variable)

This is a percentage of net revenues which equates to ~10% at the group level. Live Casino rates are lower for Tier 1 operators (e.g. William Hill) but higher for smaller operators. Slot games are usually less than 10%.

[ Net revenues = Bets - wins (GGR1) - Player Bonuses (with a cap2) - Gaming Taxes ]

Dedicated Table Fees (Fixed)

Evolution offers basic and dedicated tables. Basic agreements include access to and streaming from generic tables while more complex agreements include dedicated tables and environments, VIP services, native speaking dealers and other customisations. Evolution has ~700 tables and ~300 customers, with 80-85% tables dedicated to operators.

In addition to commissions and dedicated table fees, Evolution has smaller sources of revenue such as set-up fees, which are invoiced to new operators.

Evolution’s Platform

Evolution’s Production and Studios

Evolution invests significant time and resources in developing its offering for operators, which is a key source of its competitive advantage.

This is a labour intensive process, with each table needing six or seven people (e.g. dealers, directors, camera operators) to create the gaming production, along with a 24 hour broadcasting team (Mission Control Room) consisting of security personnel and a central operations team.

Evolution’s Platform

Evolution Product Offering

Evolution has 4 key product categories:

Live Casino: Three games drive the majority of casino revenues including Blackjack (popular in the US), Roulette (popular in Europe) and Baccarat (popular in Asia).

Live Casino Offer

Live Game Shows: Evolution pioneered this newer format which is primarily used as a conversion and cross sell tool to encourage bettors to opt for higher margin table games, further differentiating Evolution from other providers.

First person Random Number Generator (RNG): An RNG/Live Casino hybrid game which also has a “Go Live” button to upsell players to the live version of a game.

Slots: While not a historically a big source of revenue, the acquisitions of NetEnt and BTG games will increase Evolution’s exposure to this segment. Slots are a separate option in the virtual lobby (home screen where players can pick what game they want to play) which now gives Evolution more real estate across a player’s gaming experience.

Evolution’s Moat and Opportunity

Evolution’s Moat

An investment in Evolution implies you believe the company has a sustainable competitive advantage in the production and development of Live Casino games and content.

“Product innovation is central for Evolution’s success and our ambition is to pave the way for the entire industry by launching new ground-breaking products.” - Martin Carlesund, CEO

At its core, Live Casino competes on production quality and player engagement, not price. If there is limited player engagement and loss of players to other operators who do use Evolution, a casino operator's profitability is materially impacted. This is a volume game (players and bets) and Evolution provides the best immersive experience to drive this number higher for operators.

It’s impossible to distil Evolution’s competitive advantage down to one or two things. This is a case of a number of incremental advantages adding up to create high barriers to success.

I believe the key aspects of Evolution’s economic moat are:

Production Capability: Netflix + Vegas in one

Evolution’s Live Casino offering combines the skills of running a TV studio (with Netflix style production capability), a casino game with the detail of a land based casino, and managing a large workforce.

In creating a high quality compliant product, Evolution needs to achieve the following globally:

Have games certified by the appropriate regulatory authority

Create an intuitive user interface, provide multiple language options, enable players to interact with the host and regulate each game’s main plus side bets

Develop a system that can read gaming instruments such as card and dice, managed by a control centre in case there is an error

Fund the capex to build studios and tables, install multiple cameras, and create an ambient overall environment

Hire and train staff to perform across various games and languages

Manage the quality of the stream ensuring little to no latency for players regardless of device

Replicate this with minimal error rates across all bet spots. For context, Evolution managed 17.5 billion bet spots in 2Q21

This is not an easy task and requires complementary skillsets, the ability to operate at a fast pace and high volume with minimal errors, and a strong technical foundation. Evolution has managed to do this while satisfying operator and player needs for 15 years.

Economics for new providers are tough

Say you saw Evolution’s attractive margins and wanted a slice of that pie. Cutting its lunch is unfortunately not that simple due to 1) high initial fixed costs, 2) risk in hiring skilled personnel to create games (e.g. developers) and 3) lack of product breadth or reputation.

From a cost standpoint, small studios cost ~€1.5m per month to run, with a new studio likely to cost ~€30m and take close to a year before it could even launch just a limited selection of core games. Beyond this, deals with operators also take six to twelve months to close meaning a new provider is out ~€50m before they start to generate any revenue.

This is assuming casino operators would be happy to go with your limited game suite of products that risk them losing players to other operators that are utilising Evolution. An unlikely outcome.

Operator Risk in going it alone

Given the ~10% GGR payouts and Evolution’s high margins, it may be tempting for casino operators to attempt to insource game creation. Assuming capital isn’t a constraint, operators still face material risk in executing to Evolution’s high standard given it has built up capability and reputation over many years. Player engagement is the key metric for operators, if an operator’s product is inferior, the GGR loss from this can be significant as players switch to other operators with better games.

"While barriers to entry are relatively low, the barriers to success are considerably high."- Martin Carlesund, CEO

The above quote encapsulates Evolution’s edge and is persistently under appreciated by the market. It’s easy to predict that land based casinos or other operators with capital can set up a studio with some presenters, charge a lower price and take market share. However in practice, doing so creates the material risk of losing player mindshare and dollars to competitors with no guarantee that this can be recouped.

Rapid Pace of Product Innovation

Creating a great game that players love is as difficult as making a hit song that listeners love. Every game and song will find a certain audience that loves it, but appealing to a wide audience for a long time requires everything to come together perfectly. If any one element is off it can turn a song or game from a hit to a miss. All of the small things add up and must be balanced against each other. - Todd Haushalter

Evolution’s focus on product development has seen it accelerate its pace of game releases over the last few years. Evolution is releasing eight to ten games per year whereas competitors are releasing one to two. This is a sizeable difference as one provider gives operators three to four times the opportunity to market new games and help with customer acquisition and marketing campaigns all while having materially higher levels of engagement.

Evolution’s Game Launches by year

Software Development

The cost of developing a game on the software side of things requires a large software development team. Evolution has a core of hundreds of highly skilled developers, a team its organically grown over 10 years. To replicate this level of expertise not only requires dollar investment but significant time in the industry and refining the product.

Technology

Evolution has a back end platform that simultaneously handles software, hardware, video, employees and user data. The platform provides scalability and allows Evolution to expand with new studios without having to replicate software locally. It also provides easy adaptation for new markets, such as the US.

Evolution has built its own video coding solution to ensure uninterrupted video streaming in HD. After all, the last thing you want while gambling your hard earned dollars is the connection to be buffering, laggy or drop out completely.

Estimating the Total Addressable Market (TAM)

There remains large variability in outcomes given the nascent nature of the industry. While many market participants (and Evolution itself) utilise industry body H2GC’s gaming market estimates (by GGR), there remain nuances around geography and rate of regulation. As such, I take a few approaches illustrated below.3

Approach 1- Evolution’s figures (FY20 TAM)

Evolution provides TAM estimates for Live Casino every year. I looked through the annual reports from 2014 onwards and the below stood out.

The current Live Casino TAM is €5.3bn globally. This implies penetration of ~51% as per below. The table below makes some significant assumptions detailed in this footnote.4

Source: EVO disclosures, Gradient estimates Evolution quoted market figures for Europe only till FY18, where it first provided a US estimate (along with a pcp figure)

From FY20, market figures were provided on a global basis only

FY19 was the first mention of Asia as a segment (€49m of revenue), along with Evolution quoting its share of regulated markets as a percentage

Approach 2 - Top Down Global Gambling market (FY25e estimate)

Globally, I assume online casino penetration of 25% (this was 20% in FY20) or €32.6bn of a €163bn market by 2025. Of this, 30% or €12.2bn is forecast to be live casino, with the balance RNG. This implies a live casino CAGR of ~18.2% for FY20-25e.

The market for Live Casino (outside Europe) remains nascent, and as such these forecasts have a wide range of outcomes around them. In fact, having combed through a stack of sell side reports over the last few years, market forecasts vary widely (and have consistently been too cautious).

Global Casino market (2025 Estimates)

Approach 3 - TAM by Geography

Growth rates vary significantly by market and regulatory regime. Europe is the most mature with medium term incremental growth driven by the US deregulating and Asia more broadly. Beyond this, Latin America (Brazil and Mexico) are longer term growth drivers.

Europe

Europe is Evolution’s most mature market and has been at the forefront of gambling and gaming deregulation. Online casino has ~50% share with Live Casino/RNG at a 30%/70% split. In 2020, the online casino market was ~€10.5bn, with Evolution having ~60% market share of Live Casino. While Europe grew at a ~27% CAGR from FY15-20, I still expect ~20% CAGR out to 2025, implying a Live Casino market of ~€8.5bn.

United States

Flutter Entertainment (FLTR.LN) recently released a €1.1bn5 online casino TAM for every 5% of regulated US population implying a fully regulated TAM of €21bn, resulting in a €2.1bn TAM for Evolution on a 10% take rate. It also booked €48.8m of North American revenue in 1H21. Assuming an accelerated run rate to €100m for the balance of FY21 implies mature TAM penetration of 4.8%. Note, the actual pace of revenue growth will be largely dictated by the pace of regulatory outcomes on a state by state basis. Playtech estimates the US iGaming market (GGR) to be €4.5bn by 2023. A 25% CAGR from 2023 to 2025 implies a market of ~€7bn.

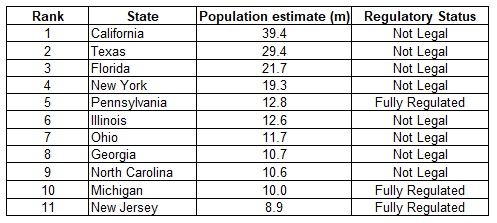

Current regulated states in the US include New Jersey, Pennsylvania and Michigan.

Top 11 US States by Population and Regulatory Status

Asia

Asia is a growing market but is mostly unregulated creating potential future opportunity. Online penetration is ~5% compared to Europe at 46%, while the land based market is €46bn.

Using Europe’s offline to online development as a proxy, Asia could have potential to be a €30bn market, implying €3bn TAM for Evolution and 7.9% penetration on a 1H21 revenue run rate of €118.9m.

Playtech and Evolution are ~10% of the market which is different in structure to Western markets as Asia is controlled by affiliates and brand elders such as Asia Gaming. Regulation will likely be a positive for established operators such as Evolution given its expertise in navigating other regulatory regimes.

Note, that according to the company China is a “small percentage of Asian revenues”. Currently, other countries like Japan, Korea, Philippines and India are far more important for growth according to Evolution.

Growth trajectory and opportunity for reinvestment

Ongoing Product Innovation

Evolution is the market leader in Live Casino and needs to maintain its pace of innovation and product development in order to hold or increase that share, given its premium pricing.

Customer Optimisation & Data

Targeted use of data can also enable cross selling opportunities, special offers and bonuses and dictate future operator investment spend based on player profiles and game statistics.

Regulated markets

Regulation is expected to be a continuing trend in coming years, underpinned by state based regulation in the US. Post regulation, a consumer is more likely to discover Live Casino and explore casino games as a category.

Land based Casino transition

Traditional land-based casinos constitute ~83% of the total casino market today. These operators often have strong brands and loyal high frequency customers. Growth for land-based casinos is low and more operators are seeking an online digital strategy to continue to grow. Live Casino can be seen as the natural bridge connecting land-based and online operations with Evolution the natural partner for these customers.

Scientific Games Deal a potential game changer

On May 27 2021, Evolution announced an exclusive agreement with Scientific Games to make its live online Lightning Roulette game available as a physical game in land-based casinos worldwide. It will be the first Evolution game (other than Dual Play Roulette and Baccarat games which are tables that are streamed from land-based casinos tables) to make the transition from live to land-based.

Scientific Games now has the right to sell land based Lightning Roulette to other casinos. Given the strength of Evolution’s IP, this could create further opportunities to expand its reach to the offline world.

The Competition

"…everything we do is about one thing: to expand the gap to competition and strengthen our market leadership."- Martin Carlesund, CEO

“I believe that some of the toughest competition we face are other forms of online entertainment. Increases in our volume is partly because we have been able to develop new games that have attracted completely new groups of players.” Martin Carlesund, CEO

CEO Martin Carlesund sounds eerily like Reed Hastings with the above quote. It’s important to re-emphasize that the entry barriers to Live Casino are relatively low, but few companies have achieved success. Live Casino demands a high level of operating capability, and a single broad based technical solution is not sufficient to build a satisfactory offering.

Playtech

Evolution and Playtech (PTEC.LN) were the two pioneers of live casino in the 2000s. While Evolution had a singular focus on live casino, Playtech hedged its bets across table games, poker, sports betting, back end platforms and land based slots. This allowed Evolution to gain market share and a product lead in live casino that it would never relinquish.

Playtech employs a bundle and takes a percentage fee across its product suite with a charge for the fixed costs of Live Casino.

Pragmatic Play

A newer competitor I came across with what appears to be a solid product is Pragmatic Play, a private company established in 2015 and owned by the IBID group. The company offers a full offering with slots, lottery games and is building out a good Live Casino offering. Revenue numbers are hard to come by but some estimates place it in the ~$2mn region making it a tiny player in comparison to Evolution at this point.

The Verdict

“To be honest, Pragmatic and Playtech come in very, very cheap. They really try to cater to our needs. But then the performance metrics aren't there. So if you look at clicks, for example, if I put an Evolution game right next to a Playtech game, I've got tenfold, even more in some cases. And I'm talking apples for apples.”- Industry Expert

Regulation

Licensing and Regulation

The gaming industry is regulated at a national or a regional level. Many countries have regulations for land-based casinos that are not applied to online gaming.

Regulation is an important growth factor for the online casino market, because it brings more potential end users and gives operators greater opportunities to promote the product. - Evolution Annual Reports

There are three types of regulated markets, described below.

White (Fully regulated): e.g. UK,

Black (totally illegal) e.g. Turkey, China

Grey (unclear regulatory framework) e.g. Eastern Europe. Companies typically operate through sports betting and gaming licenses issued in Malta. Under EU law, these licenses are effective in all EU member countries due to the freedom of movement within the EU

Evolution has attained over 10 licenses needed to offer its services in their respective geographies. Evolution also has an MGA license, which is a Malta gaming license and can be used in grey markets.

Regulatory requirements can include (but not limited to) licenses, KYC/AML compliance, and minimum betting standards that lend themselves to favouring larger operators and a higher quality industry structure.

Evolution Licenses and Certifications

As a general rule, regulation is positive for casino operators and suppliers. If regulatory requirements increase, it’s likely that scaled players such as Evolution will benefit given 1) cost of implementation and 2) experience in dealing with regulatory bodies globally.

It's not often that they [markets] go from non-regulated to being black, it's more that they want to regulate it- Industry Participant

Europe

Most of Europe is either regulated, or will become regulated over the next five years.

US

Five states currently regulate online casinos (Delaware, New Jersey, Pennsylvania , West Virginia and Michigan). Evolution has studios operating in both New Jersey and Pennsylvania and recently opened a third studio in Michigan. Connecticut passed legislation earlier this year and Evolution is planning for that market to open later in the American Fall.

Due to the Federal Wire Act, Live casino products have to be offered from a live studio local to that state.

Other states that could regulate in the next year or two include Indiana, Illinois and Virginia, as well as Ontario in Canada.

In addition to receiving a license to offer games, operators also must get each individual game approved by the regulating body.

Asia

Asia is broadly unregulated (grey), and China is a black market. Key markets for Evolution include India, Thailand, Vietnam, and Japan.

Evolution says its Asia revenues are being generated from increased focus by existing licensees (i.e. already operating under a Malta or Curaçao license) rather than being through a structure of Asian-specific aggregators or agents. Asia is Evolution’s most opaque market with regulatory risks hardest to assess.

Capital Allocation and Financials

Capital Allocation

It’s hard to fault Evolution’s historical capital allocation strategy, given its strong top line growth rates and even stronger financial health.

Dividend & Reinvestment Rates

Some investors question Evolution’s dividend policy of paying out a minimum dividend of 50% of net profit over time ( a historical policy as most Swedish companies pay out dividends). On a theoretical basis, I would agree given the large market opportunity up for grabs.

However in practice 1) Evolution has grown at supernormal rates for the last decade with management having to manage the growth and development of the organisation to meet this challenge, a difficult task; and 2) Evolution is well capitalised to fund future growth.

“If five US states were to regulate tomorrow, we could start construction on studios”- Evolution management

M&A

Evolution recently acquired Slots providers NetEnt (December 2020 and Big Time Gaming (April 2021). I haven’t specifically explored the operational synergies between Slots and Live Casino in this report. Slots make up the majority of the online casino market (albeit with slower growth and more fragmentation) and presents EVO with the opportunity to further leverage its scale and cross selling capability.

“Now with NetEnt as part of Evolution, we will blend NetEnt player favorites into the world of Live Casinos to create a new wave of games that provide players with just more truly unique entertainment experiences. Needless to say, I'm very excited about the coming game launches for 2021 for both Evolution Live and Slots.” - Martin Carlesund

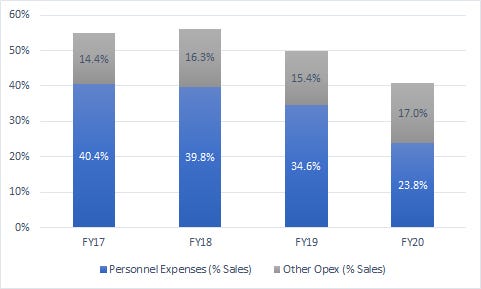

Financials

Evolution has some of the strongest financials I’ve seen. The kicker for such high EBITDA and operating margins is not having to spend on sales and marketing (1% of employees work in sales and marketing). As a B2B provider, the operator (i.e. Evolution’s customers) takes on this burden.

The company has been conservatively run with no debt on the balance sheet. Free cash flow (FCF) has grown from €12 mill in 2015 to €279 mill in 2020. FCF conversion (of net income) on average is about 90% and was 97% in FY20. ROEs have averaged ~50% on tangible assets over the last five years. In other words, the business has been highly profitable and efficient.

I’ll let the charts below speak for themselves.

Costs & Capex

Evolution's largest cost is its staff. It currently has 11,311 employees, the majority of which are dealers located in its studios globally. Personnel expenses rise as Evolution launches new games as studios, but with strong operating leverage given the scalability of Live Casino.

Other opex primarily relates to consumable equipment, communication costs, consultant fees and royalties.

Capex needs are light and are roughly evenly split between intangibles ( new game development, platform improvements) and PP&E (new studio space and premises, new gaming tables, servers and computer equipment). I forecast capex to increase by >70% (from a low base) in FY21e as Evolution further expands into the US and Asia, but given its top line growth, capital intensity will still decline by 70bps.

Management & Incentives

Jens Von Bahr and Fredrik Österberg founded the company in 2006. They remain on the board and control ~13% of the outstanding shares.

CEO Martin Carlesund holds a €40m stake in the company with another 2.175m eligible warrants and 1m options. Chief Product Officer Todd Haushalter has a €8.4m stake in the company with a further 210,000 eligible warrants.

Senior executives are remunerated using a combination of:

Fixed salary: annual base salary

Variable compensation: cash based and paid on a predetermined and measurable performance criteria aimed at promoting the company’s long term value creation. Payments can be 0-50% of annual base salary.

Incentive Programmes: Aimed to increase alignment between executives and shareholders.

2021/24: Max of 5m warrants to be issued at SEK1,113.80 to 20 March 2024.

2020/23: Max of 4m warrants to be issued at SEK 373.90 to 31 March 2023. The dilution effect is expected to be 1.9%.

2018/21: Max of 3,088,510 warrants to be issued at SEK 141.06. The dilution effect is expected to be 0.8%.

Evolution Share Register (FY20)

Culture

A final point to note is on Evolution’s culture, which it believes is a point of difference. CEO Martin Carlesund drives an organization where employees believe in the company mission. The company believes its greatest risk is complacency and want to avoid resting on their laurels as much as possible.

“We are crazy, paranoid; we really want to be better every day. We want to be the best company in the world. How are we going to get there? If you lose that, you should quit.” - Martin Carlesund

Some facts:

Employee turnover decreased for the third year in a row in 2020.

45% females in senior management roles

50/50 gender split in terms of studio leads

“At Evolution, we consider diversity a strategic advantage and a key asset.”

Valuation

Evolution is highly profitable and trades at a premium 45x FY21 FCF (48x PE) due to its high growth rate and market opportunity. There has been significant multiple expansion over the last 18 months as the market has caught on the quality of the business.

I am not a fan of relative valuation, especially as a long term investor. Explicitly forecasting out cash flows in such a nascent industry is also fraught with risk and provides false precision. As such, I rely on a reverse DCF6 under varying assumptions to provide some context.

This methodology implies that Evolution needs to average a 11.5% revenue CAGR from FY22e-FY30e to justify today’s stock price. It has averaged a revenue CAGR of 49% over the last five years and 48.7% over the last ten years.

My bear case is a doubling of revenues from €1,082m (FY21e) to €2,164m (FY30e) at an 8% CAGR. While this seems aggressive at first glance, the industry will likely grow at close to ~20% pa during this time. As such, this bear case discounts either 1) adverse regulatory outcomes and/or 2) material loss of market share.

Given Evolution’s already high operating margins, there is very little incremental operating leverage accounted for within these forecasts.

Upside optionality not explicitly forecast also exists from the synergies in slot game enhancement and the new land based deal with Scientific Games.

Where could I be wrong?

The bear thesis on Evolution lies in getting the growth trajectory and hence the long term earnings power of the business wrong. The company has produced a phenomenal 49%/61% revenue/EBITDA 5 year CAGR. As such, it trades on a premium multiple given its high quality earnings base and robust outlook. Any impairment of this is likely to result in short term share price disappointment.

I see three key areas of risk.

Competition or Insourcing

Evolution is a best in class provider that gives its customers the best ROI despite its premium pricing. Evolution has dominant share in the mature Europe market and is well placed to benefit from growth in both the US and Asia.

Gambling operators (i.e. Evolution’s customers) can potentially insource this function, however my research overwhelmingly shows that while technical barriers to entry are low, barriers to success are extremely high. The most important thing for operators is player engagement and if operators move off Evolution’s products they will lose share to competitors given players have no brand loyalty when it comes to online casino. It is simply not in an operator’s interest to switch from Evolution.

Adverse Regulatory Outcomes

With the European market maturing at 50% online penetration, Evolution’s next step change in growth will likely come from the US and to a lesser extent Asia and Latin America. With the US, any adverse delay in regulatory outcomes could halt Evolution’s growth trajectory and change market perception. If any Asian markets go from grey to black, this could also impact Evolution’s second leg of growth beyond the US.

Key Person Risk

Evolution faces key person risk from Chief Product Officer Todd Haushalter, who is a key reason for its product development pace, expertise and competitive advantage.

Conclusion

Evolution is a high quality company with ROEs north of 30% and a long runway of growth ahead. Unfortunately the market has realised this, with the shares trading at a premium valuation to where they did even a year ago.

In spite of this, the prospects for Evolution remain strong, underpinned by a nascent but rapidly growing market, superior product experience and focused management team.

An investment in Evolution comes down to a belief that current trends will continue and the company will continue to maintain its market share lead along with best in class reputation. Even with a strong appreciation in the equity, I believe today’s risk/reward is favourable for the long term investor.

Further Resources

There are already some excellent writeups on Evolution available as well as other resources to get up to speed on the company. A selection is provided below.

Magnus Andersson’s writings (Part 1, Part 2, Part 3)

iGaming NEXT podcast with Todd Haushalter

Gaming Intelligence Interview with Martin Carlesund

Disclaimer

This report is intended for informational purposes only. This report is under no circumstances intended to be used or considered as financial or investment advice, a recommendation or an offer to sell, or a solicitation of any offer to buy any securities or other form of financial asset.

Gross gaming revenue

Usually 5-10%

Note, the TAM focus is Live Casino given Evolution’s market position and the increased maturity (mid single digit growth) and fragmentation of the online Slots market.

GGR Revenue Share of 50% is derived from 2019 Europe numbers.

US$1.3bn in presentation

Key DCF Assumptions: RFR: 3%, ERP: 5.5%, WACC: 7.6%, LT growth rate: 2.5%, terminal multiple 19.6x

Man, this is beautiful. Well done, glad I found you